January 17, 2018

Savings Jar: How Unpaid Work Hurts Older Women's Retirement Savings

By Dr. Teresa Ghilarducci

The Federal Bureau of Labor Statistics recently reported that there was a 3.3% unemployment rate for workers age 55 and older during the month of December 2017.

While this aggregate number is impressively low, the reality is that many older workers have low-paying jobs that don’t provide retirement savings coverage. Older women are especially likely to be in low-paying jobs, in part due to the unequal division of household work.

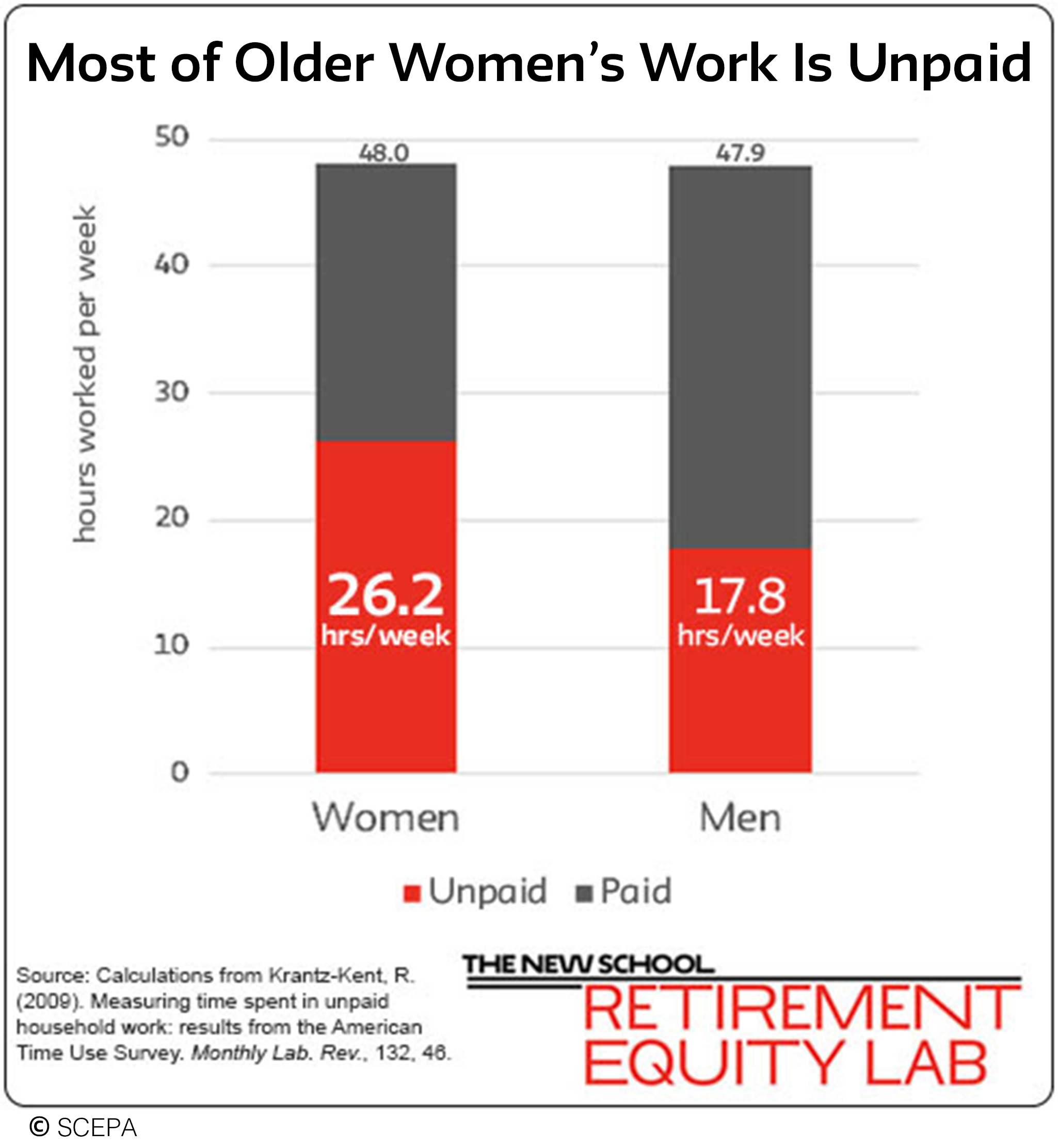

Both men and women ages 55-64 spend the same amount of time working each week — 47.9 hours a week for men and 48 hours a week for women — including both paid work in the labor market and unpaid household work. But of this total, men spend more time in paid work than women — 30.1 hours for men vs 21.8 hours for women.

Women spend more time on unpaid household work such as food preparation, cleaning, care giving, etc. Not only do older women get paid for a smaller share of their working time, in the labor market they are more likely than men to be in low-paid jobs — 38% of older women make less than $15 an hour vs 28% of men.

While older men and women have about the same low rates of access to a retirement plan at work (45% for men and 47% for women), women’s ability to save for retirement is further hurt by the combination of low hourly pay and crowd out of paid work by unpaid work. Older women have a median balance of $70,000 in their retirement accounts, compared to $106,000 for men.

To ensure all workers have a secure retirement, Congress needs to not only raise the minimum wage, but also enact Guaranteed Retirement Accounts (GRAs). GRAs provide retirement savings accounts to all workers as a supplement to an expanded Social Security program. The GRA’s $600 refundable tax credit and employer contribution ensure that even low-paid workers, a majority of whom are women, can afford to save for retirement.

© SCEPA

The Retirement Equity Lab (ReLab) at the Schwartz Center for Economic Policy Analysis’s (SCEPA), led by economist and retirement expert Teresa Ghilarducci, researches the retirement crisis that exposes millions of American workers to downward mobility in retirement.

This is an updated version of an article previously published by Public Seminar, a project at The New School for Social Research that describes itself as “an intellectual commons for analysis, critique, and debate.” Public Seminar publishes articles it judges useful, constructive, illuminating, or thought-provoking contributions to the conversation of the times.